What's the value of a podcast exclusive?

How platforms use hits to win the market

A couple of interesting articles dropped in the last week looking at different elements of Spotify’s podcasting business.

The first is a blog post from the company talking about them making more of their owned shows Spotify exclusives.

Exclusives, or the slightly weaker ‘windowed’ versions (where a show is exclusive somewhere for a little while) are important elements to help drive consumption on particular platforms.

They potentially drive both reach and hours. You really want to hear the Joe Rogan Experience? Then you have to listen on Spotify. If it drives people who were Apple Podcast users to use Spotify, maybe for the first time for their podcasting, then it perhaps starts the process of them moving over to make Spotify their default podcasting app.

If you’re a regular user of Spotify, seeing new episodes of Joe Rogan, and other exclusive shows may also keep you locked in and extend your listening (driving hours consumed for the company).

As well as specific titles that people seek out on a platform, there can also be the friction they notice - “oh, it’s a pain that some of my shows are in one place, and I have to flip apps, I might as well listen to everything on Spotify”.

This works only if the platform, Spotify in this case, has the lion’s share of exclusives. Otherwise a user still has to use multiple apps, so it doesn’t quite push them into lock in.

Looking at Spotify, they’ve certainly been the most aggressive. Local originals - like GIANT in the UK, the acquisition of big podcast companies (Gimlet, Parcast, Ringer and making some shows exclusive) and then doing deals with some big shows - Joe Rogan, Armchair Expert, Call Her Daddy - to get them onto Spotify exclusively.

Outside of Spotify there are some exclusives on things like Audible or BBC Sounds but they lack the momentum Spotify has with its material. To achieve that is an expensive business - they’re probably on the way to having spent $1bn on podcast content.

The challenge with any content is keeping it popular and ensuring there’s a good pipeline of new stuff on its way.

Spotify’s competitor Amazon Music is keen to get into this game too, and not allow Spotify to run away with all the talent. Its got involved with SmartLess, the weekly interview show with actors Will Arnett, Jason Bateman and Sean Hayes. They’ve paid around $25m a year (for three years) for windowing rights and a sort of first-look deal for new shows from the gang. It’s a really popular show at the moment, will it last? Will they fall out? Will one sign a TV deal that means they can’t do the podcast any more? Will some (or all) be cancelled after a previous misdemeanour arises?

All these content deals have a certain amount of uncertainty built in. But if the game is about trying to corner the market on the big shows, there’s probably not that much time spent worrying about the future.

The second article was a piece in Business Insider looking at the relative performance of Gimlet, a network that Spotify acquired that kicked off a lot of podcast merger and acquisition activity.

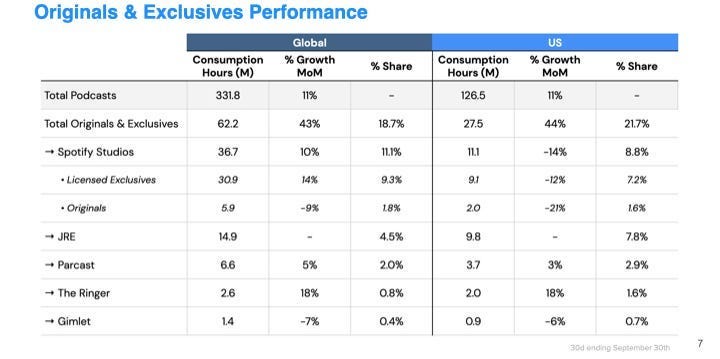

They’d gotten hold of some internal Spotify data from September last year which broke down the amount of listening to podcasts on Spotify, and their own content’s performance:

It’s interesting to see hours consumed rather than ‘downloads’. As a streamer it’s a metric that’s pretty exclusive to Spotify. They know what you’ve actually listened to, rather than just adding up downloads. It’s also important to remember that this is a year old, so it’s likely to have changed quite a bit since then.

But as a snapshot it’s fun to dive into. It shows around 20% of the podcast consumption comes from their own programming - the rest from the long tail of the world’s RSS-driven podcast shows.

It also shows the hours-consumed value of hit shows rather than building out your own new material. At nearly 15m hours, the Joe Rogan Experience was a quarter of their O&E (originals and exclusives) and this was before the show became exclusive to the network and stopped being on YouTube - that happened at the end of 2020.

Indeed the other ‘licensed exclusives’ were around half of O&E, so when combined - buy in’s accounted for 73%, whilst Spotify’s production companies and their own originals accounted for the smaller remainder.

When you look at the hours generated by something like Gimlet (that they paid $230m for), Joe Rogan at $100m a year seems like a much better deal.

Using these deals to buy market share is one thing, but they’re also buying inventory to sell to advertisers, and I guess it’s premium inventory on premium shows.

In the Business Insider piece, it alludes to an interesting problem for Spotify. Owning the platform means that you can promote your material as much as you like. But when you’ve got so much material (including all the many shows created by Parcast, Ringer and Gimlet) you probably haven’t got enough room to really give Spotify promo value to your acquisitions. It’s probably much easier to plug Joe Rogan than to take a gamble on a more niche Parcast show.

Media has always been in the hits business. With the big shows generating the big money. It looks like podcasting at scale is perhaps no different.

Creating a hit vs farming exclusives

The thing that a lot of these Spotify big money transfers have in common is that they grew their audience in the open podcasting world - where they were available, to coin a phrase, ‘wherever you get your podcasts’.

And that makes sense. The big value of exclusives is using the star power to change user behaviour. Yes, you may discover an exclusive show on the app you regularly use, but it’s not really making you change behaviour, indeed you probably give the app no real credit for that exclusive show - I bet most people assume it’s in other places too. At best they may stop you entirely abandoning an app when you’ve been flirting with switching to a new one.

I think this is a challenge for something like BBC Sounds.

The other week I’d seen a tweet mentioning that the excellent CBBC programme Operation Ouch had a podcast spin off. This made me a little worried, as at Fun Kids we make a load of kids podcasts and any new shows in what I see as my genre, gets me concerned.

But it turns out that Operation Ouch! The Podcast of Everything, is a BBC Sounds exclusive, so it won’t compete with my kids podcasts where we appear - like Spotify and Apple Podcasts. I then stumbled over the fact that they’d launched a whole load of other kids shows at the same time including a new Horrible Histories podcast and Tales from Mallory Towers - two TV spin-offs from great brands.

All this is prime competition for my listeners’ ears but thankfully it’s locked away on BBC Sounds and isn’t even promoted on the CBBC website for each of those TV shows. The sheer volume of BBC audio content (and that I imagine the kids stuff isn’t high up the promo list) means it’s also quite hard to find on BBC sounds (Home - scroll down to Categories - click View All - scroll down to Browse All Speech - click Children’s).

I’m not particularly having a go at BBC Sounds. If you were looking for a new Parcast series on Spotify you’d face the similar problem - the one I talk about above. Is it worth creating all of this great content if you can’t show it to people to get them to listen to it? Where there is far more certainty and financial value is in picking up a hit, with the show’s momentum doing a lot of the discovery work for you.

What I also think it means is that broadcasters, or production companies can probably be too quick in making things exclusives. Hiding them away when they aren’t significantly famous doesn’t probably generate you that much value.

If Horrible Histories Season 1 became a smash hit because people discovered it in all the public places - like Apple Podcasts and Spotify - wouldn’t Season 2 exclusive on BBC Sounds be more of a draw?

Enjoyed this? Get posts in your inbox each week by subscribing for free: